5.3. Evaluation Metrics#

Quantification metrics measure the discrepancy between the estimated prevalence vector \(\hat{p}\) and the true prevalence vector \(p\). Unlike classification metrics, they operate on aggregate probability vectors — not on individual predictions.

All metrics in mlquantify follow the same calling convention:

error = MetricName(true_prevalences, predicted_prevalences)

Both arguments can be:

A flat array of true class labels (

y_true), orA prevalence dict/array returned by

quantifier.predict(X).

mlquantify automatically converts true labels to prevalences using

get_prev_from_labels when needed.

5.3.1. Absolute Error Metrics#

5.3.1.1. AE and MAE — (Mean) Absolute Error#

AE computes the mean absolute difference per class over a single

sample. MAE averages AE over multiple samples (from a protocol).

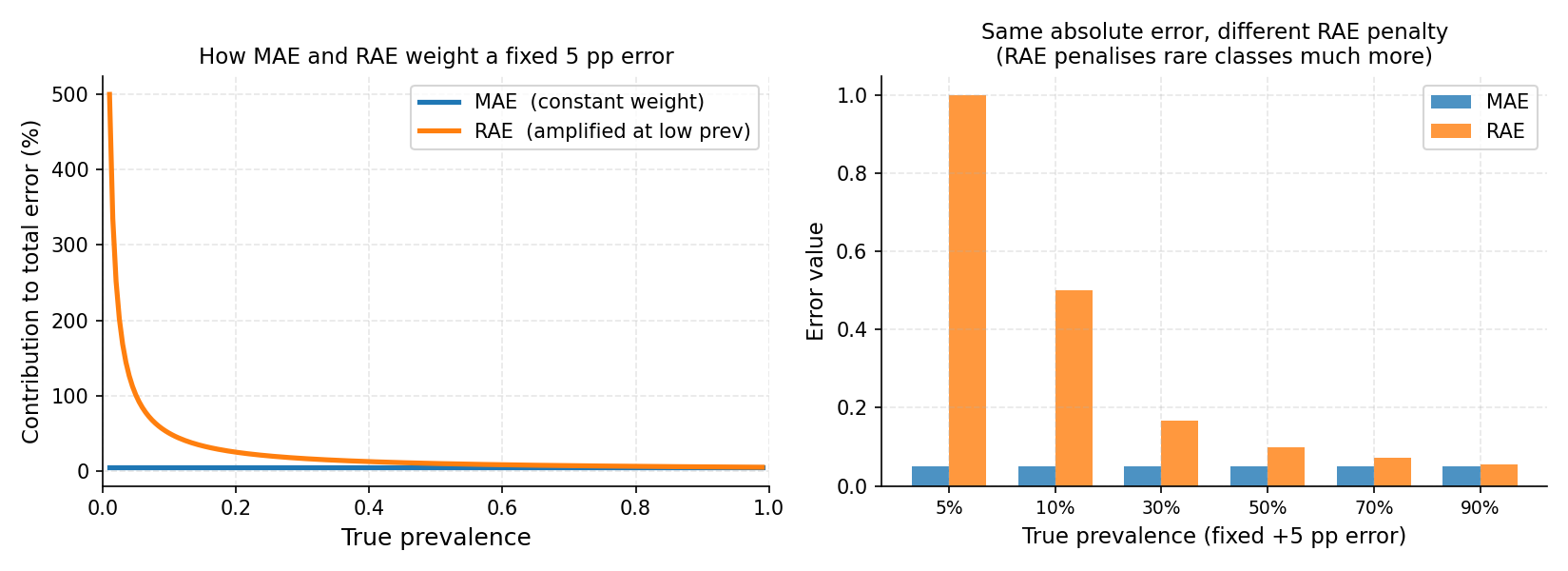

When to use: MAE is the standard metric for quantification evaluation. It is interpretable (the average error in prevalence units, e.g. 0.05 means “off by 5 percentage points on average”), symmetric, and gives equal weight to all classes and prevalence levels.

Left: for a fixed 5 percentage-point absolute error, MAE assigns equal weight regardless of the true prevalence (flat blue line), while RAE’s contribution grows steeply as prevalence approaches zero (orange curve). Right: the same 5 pp absolute error applied at different prevalence levels — RAE imposes a much heavier penalty at 5% and 10% prevalence, reflecting that a 5 pp error is far more significant when the true value is 5% than 50%.#

from mlquantify.metrics import MAE, AE

from mlquantify.utils import get_prev_from_labels

import numpy as np

y_true = np.array([0, 0, 1, 0, 1, 1, 0, 0, 0, 1])

y_pred = {0: 0.62, 1: 0.38}

true_prev = get_prev_from_labels(y_true)

print(AE(true_prev, y_pred)) # single-sample AE

# 0.02

# Over multiple protocol samples

errors = [AE(get_prev_from_labels(y_s), q.predict(X_s))

for X_s, y_s in samples]

print(MAE(errors)) # mean over all samples

5.3.1.2. SE and MSE — (Mean) Squared Error#

SE penalises large errors more severely than AE (quadratic vs

linear). Use MSE when large deviations are especially harmful.

from mlquantify.metrics import MSE

print(MSE(true_prev, y_pred))

5.3.2. Relative Error Metrics#

5.3.2.1. RAE and NRAE — (Normalised) Relative Absolute Error#

where \(\varepsilon\) is a small smoothing constant.

When to use: RAE amplifies errors at low prevalences. An error of 5 percentage points matters much more at 5% prevalence than at 50%. Use RAE when rare classes are important (e.g. rare disease detection, fraud detection).

NRAE normalises RAE to \([0, 1]\) so it is comparable across

datasets with different numbers of classes.

from mlquantify.metrics import RAE, NRAE

print(RAE(true_prev, y_pred))

print(NRAE(true_prev, y_pred))

5.3.2.2. NAE — Normalised Absolute Error#

NAE normalises AE by the number of classes so results are comparable

across different multiclass settings.

5.3.3. Divergence Metrics#

5.3.3.1. KLD and NKLD — (Normalised) Kullback-Leibler Divergence#

KLD measures the information loss when using \(\hat{p}\) to approximate \(p\). It penalises zero-probability predictions asymptotically (use the smoothed version internally).

When to use: KLD is used when prevalences represent probability

distributions and you care about calibration. It is asymmetric — the true

and estimated distributions are not interchangeable — so the convention

matters (KLD(true, pred)). NKLD normalises to \([0, 1]\).

from mlquantify.metrics import KLD, NKLD

print(KLD(true_prev, y_pred))

print(NKLD(true_prev, y_pred))

5.3.4. Ordinal Metrics#

5.3.4.1. NMD — Normalised Match Distance#

NMD is designed for ordinal quantification tasks where classes

have a natural order (e.g. severity levels: mild < moderate < severe). It

measures the earth-mover distance between the CDFs of \(p\) and

\(\hat{p}\).

When to use: Use NMD when your classes are ordered and the distance between adjacent classes matters. For non-ordinal problems, AE or KLD are more appropriate.

from mlquantify.metrics import NMD

# Ordinal classes: 0 < 1 < 2

true_prev = [0.5, 0.3, 0.2]

pred_prev = [0.4, 0.4, 0.2]

print(NMD(true_prev, pred_prev))

5.3.4.2. RNOD — Relative Normalised Order Distance#

RNOD is a relative version of NMD that amplifies errors at low

prevalences — analogous to RAE for ordinal settings.

5.3.5. Distribution Distance Metrics#

The following functions also serve as loss functions in distribution-matching quantifiers:

Function |

Description |

|---|---|

|

Hellinger distance between two distributions. \(\in [0, 1]\). |

|

TopSoe (Jensen-Shannon-like) divergence. |

|

Probabilistic symmetric chi-squared divergence. |

|

Squared Euclidean distance. |

These are available both in standard numpy and JAX-compatible variants

(hellinger_jax, etc.) for gradient-based optimisation.

5.3.6. Choosing a Metric#

Metric |

Use when |

|---|---|

MAE |

Default. Most papers report MAE. Easy to interpret. |

RAE |

Rare classes matter; you want errors at low prevalences amplified. |

KLD / NKLD |

Probabilistic calibration of the prevalence vector matters. |

MSE |

Large estimation errors are especially harmful. |

NMD |

Classes have a natural order (ordinal quantification). |

NRAE / NAE / NKLD |

Comparing results across datasets with different class counts. |

Full evaluation example:

from mlquantify.model_selection import APP

from mlquantify.metrics import MAE, RAE, NKLD

from mlquantify.utils import get_prev_from_labels

from mlquantify.likelihood import EMQ

from sklearn.linear_model import LogisticRegression

from sklearn.datasets import make_classification

from sklearn.model_selection import train_test_split

import numpy as np

X, y = make_classification(n_samples=2000, weights=[0.8, 0.2],

random_state=42)

X_train, X_test, y_train, y_test = train_test_split(

X, y, test_size=0.5, random_state=42)

q = EMQ(LogisticRegression())

q.fit(X_train, y_train)

protocol = APP(batch_size=100, n_prevalences=21, repeats=10,

random_state=42)

maes, raes, nklds = [], [], []

for idx in protocol.split(X_test, y_test):

X_s, y_s = X_test[idx], y_test[idx]

tp = get_prev_from_labels(y_s)

pp = q.predict(X_s)

maes.append(MAE(tp, pp))

raes.append(RAE(tp, pp))

nklds.append(NKLD(tp, pp))

print(f"MAE: {np.mean(maes):.4f}")

print(f"RAE: {np.mean(raes):.4f}")

print(f"NKLD: {np.mean(nklds):.4f}")

Evaluation metrics for quantification assess the accuracy of estimated class prevalences against true prevalences. These metrics are crucial for understanding how well a quantifier performs, especially under distributional shifts.

The library includes several widely used evaluation metrics:

Metric |

Description |

|---|---|

Normalized Match Distance |

|

Relative Normalized Overall Deviation |

|

Variance Shift Error |

|

Cramér-von Mises L1 Distance |

|

Absolute Error |

|

Squared Error |

|

Mean Absolute Error |

|

Mean Squared Error |

|

Kullback-Leibler Divergence |

|

Relative Absolute Error |

|

Normalized Absolute Error |

|

Normalized Relative Absolute Error |

|

Normalized Kullback-Leibler Divergence |

5.4. Single Label Quantification (SLQ) Metrics#

5.4.1. AE (Absolute Error)#

Parameters:

\(p\): array-like, shape (n_classes,) True prevalence (distribution of classes).

\(\hat{p}\): array-like, shape (n_classes,) Estimated prevalence.

AE calculates the simple absolute error across classes:

Its primary strength is transparency and ease of interpretation.

5.4.2. SE (Squared Error)#

Parameters:

\(p\): array-like, shape (n_classes,) True prevalence.

\(\hat{p}\): array-like, shape (n_classes,) Estimated prevalence.

SE is the sum of squared differences:

This penalizes larger errors more heavily, making outlier mistakes more obvious.

5.4.3. MAE (Mean Absolute Error)#

Parameters:

\(p\): array-like, shape (n_classes,) True prevalence.

\(\hat{p}\): array-like, shape (n_classes,) Estimated prevalence.

MAE averages the absolute errors over all classes:

It offers a normalized perspective, useful for comparing performances across datasets.

5.4.4. MSE (Mean Squared Error)#

Parameters:

\(p\): array-like, shape (n_classes,) True prevalence.

\(\hat{p}\): array-like, shape (n_classes,) Estimated prevalence.

MSE averages the squared errors:

Ideal for highlighting large deviations in prevalence estimation.

5.4.5. KLD (Kullback-Leibler Divergence)#

Parameters:

\(p\): array-like, shape (n_classes,) True prevalence.

\(\hat{p}\): array-like, shape (n_classes,) Estimated prevalence.

KLD measures the information loss between distributions:

Its key advantage is sensitivity to wrong predictions where the true prevalence is high.

5.4.6. RAE (Relative Absolute Error)#

Parameters:

\(p\): array-like, shape (n_classes,) True prevalence.

\(\hat{p}\): array-like, shape (n_classes,) Estimated prevalence.

\(\epsilon\): float, optional (default=1e-12) Small constant to ensure numerical stability.

RAE scales the absolute error by true prevalence:

This is beneficial for identifying relative impact in imbalanced scenarios.

5.4.7. NAE (Normalized Absolute Error)#

Parameters:

\(p\): array-like, shape (n_classes,) True prevalence.

\(\hat{p}\): array-like, shape (n_classes,) Estimated prevalence.

NAE normalizes the absolute error:

Best used for ensuring error scale invariance.

5.4.8. NRAE (Normalized Relative Absolute Error)#

Parameters:

\(p\): array-like, shape (n_classes,) True prevalence.

\(\hat{p}\): array-like, shape (n_classes,) Estimated prevalence.

\(\epsilon\): float, optional (default=1e-12) Small constant for numerical stability.

NRAE further normalizes relative errors:

This balances error measurement between true and estimated values.

5.4.9. NKLD (Normalized Kullback-Leibler Divergence)#

Parameters:

\(p\): array-like, shape (n_classes,) True prevalence.

\(\hat{p}\): array-like, shape (n_classes,) Estimated prevalence.

\(\epsilon\): float, optional (default=1e-12) Small constant for numerical stability.

NKLD outputs a normalized form of KLD:

This makes it robust for comparing across distinct sample sizes.

5.5. Regression-Based Quantification (RQ) Metrics#

5.5.1. VSE (Variance Shift Error)#

Parameters:

\(p\): array-like, shape (n_classes,) True prevalence.

\(\hat{p}\): array-like, shape (n_classes,) Estimated prevalence.

The Variance Shift Error quantifies the discrepancy between the variance of true and estimated distributions:

This metric emphasizes changes in dispersion, which is useful for detecting model bias towards certain classes.

5.5.2. CvM_L1 (Cramér-von Mises L1 Distance)#

Parameters:

\(p\): array-like, shape (n_classes,) True prevalence.

\(\hat{p}\): array-like, shape (n_classes,) Estimated prevalence.

CvM_L1 compares cumulative distributions using the L1 norm:

where (F_p(c)) is the cumulative distribution. Its advantage lies in capturing distributional differences beyond pointwise errors.

5.6. Ordinal Quantification (OQ) Metrics#

5.6.1. NMD (Normalized Match Distance)#

Parameters:

\(p\): array-like, shape (n_classes,) True prevalence.

\(\hat{p}\): array-like, shape (n_classes,) Estimated prevalence.

The NMD metric quantifies the normalized difference between two prevalence distributions:

where ( p(c) ) is the true prevalence and ( hat{p}(c) ) is the estimated. The advantage of NMD is its straightforward interpretability and normalization, making it ideal for comparing different quantification methods.

5.6.2. RNOD (Relative Normalized Overall Deviation)#

Parameters:

\(p\): array-like, shape (n_classes,) True prevalence.

\(\hat{p}\): array-like, shape (n_classes,) Estimated prevalence.

\(\epsilon\): float, optional (default=1e-12) Small constant to ensure numerical stability.

RNOD measures the proportional deviation between the true and estimated prevalence, particularly highlighting errors in rare classes:

Its benefit is in handling imbalanced distributions by reducing the influence of dominant classes.